Zero Intolerance: Audit Committees Home On The Range

By

Professor Michael Mainelli

Published by Financial World, IFS School of Finance (August/September 2014), page 61.

Zero Intolerance: Audit Committees Home On The Range

In the wake of financial crises since 2007, a lot of work has gone into suggestions for providing more confidence in financial reporting and audit. It is nice to see two pieces of work reinforcing one another, the Financial Reporting Council’s guidance on audit committee reporting and Long Finance’s Confidence Accounting initiative.

In a speech to the Public Company Accounting Oversight Board in the USA on 19 November 2013, Stephen Haddrill, CEO of the Financial Reporting Council, pointed out that “Audit committees should now disclose significant issues considered in relation to the financial statements and how they were addressed”, and “Disclose judgement calls made for the year, and the sources of assurance and other evidence drawn upon to satisfy yourselves of the appropriateness of the conclusion”. Equally, auditors must now explain in more detail how they assessed risks of material misstatement. International Standard on Auditing 700, “The Independent Auditor’s Report On Financial Statements”, requires auditors to articulate significant financial risks, but does not set out a format. Auditors and audit committees need a common way of communicating risk.

Long Finance’s Confidence Accounting initiative encourages companies and audit firms to use ranges, rather than discrete numbers, for major accounting entries. In a world of Confidence Accounting, the end results of audits would be presentations of distributions for major entries in the profit & loss, balance sheet, and cashflow statements. Ranges provide a fairer representation of financial results, mitigate mark-to-market effects, reduce the number of footnotes, and aid measuring audit quality over time.

There are numerous ‘judgement calls’ in financial statements - revenue recognition, tax liabilities, goodwill & intangibles, asset valuations, share-based payments, and management & performance fees. Confidence Accounting would have all of these judgement calls represented as ranges. But doesn’t this result in complexity? There are indeed complicated ways of expressing ranges. One look at ‘bell curve’ distribution functions from a typical risk package, let alone special distribution functions or cumulative frequency charts, gives an idea of how to get complex quickly.

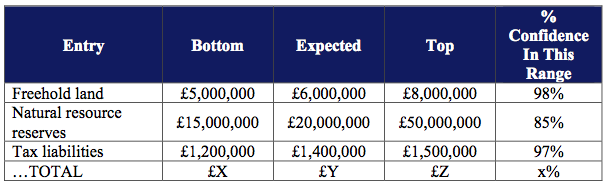

There are numerous ways of representing ranges, such as errors bars on a chart, candlestick diagrams common amongst traders, time-based fan charts for economists, and box & whisper diagrams for scientists. One of the simplest ways of representing ranges is simply to state the bottom value, the expected value, and the top value, with a judgement on the likelihood that the value is in that range – BET%. As a simple example, a value for freehold land assets might be expressed as, B: £5 million, E: £6 million, T: £8 million, with a 98% confidence the value is in that range.

Applying this to a simple natural resources company balance sheet for a few entries might produce an example table like this:

The table suggests a simple agenda for audit committees and their auditors. Proceeding line by line, the following questions naturally arise:

- this range - what are the factors that might affect bottom, expected, and top? what work have you done to assure yourself of this range and this confidence level?

- wider - what scenarios or events would materially wide the range? what has to happen to make sure the range doesn’t widen?

- narrower - what evidence or work could narrow the range?

- confidence - what are the implications of being outside the range? what else would we wish to know?

- shape - is there anything unusual about the range, e.g. a binary outcome?

- presentation - what is the right financial information about this range to provide to stakeholders?

There are many more complicated situations than the above example, e.g. derivatives in a financial institution. That said, quite a bit of most balance sheets can be discussed by audit committees and their auditors using the straightforward BET% approach. The accountancy profession is moving towards better understanding and better handling of uncertainty. Much of the tension for accountants has been generated by the discord of a single historic cost number colliding with the need for judgement. More tension has been generated when historic and current accounts collide with future-looking risk scenarios. Much of the tension is released when ranges are recognised as fundamental to any discussion about financial reporting. Formal presentations to audiences and financial reports to stakeholders should have a lot in common. Confidence should be projected to the audience through knowledge and experience. A simple approach to ranges can go a long way in helping to incorporate knowledge and experience in discussions between audit committees and their auditors. Professor Michael Mainelli is Executive Chairman of Z/Yen Group. His latest book, The Price of Fish: A New Approach to Wicked Economics and Better Decisions, written with Ian Harris, won the 2012 Independent Publisher Book Awards Finance, Investment & Economics Gold Prize.

An edited version of this article appeared as "At Home On The Range" (Confidence Accounting), Financial World, IFS School of Finance (August/September 2014), page 61.