You Can't Predict Share Prices, But You Can Spot The Odd Ones

Monday, 08 May 2006By Now&ZYen

8 May 2006

The European Union’s Markets in Financial Instruments Directive (MiFID) Article 21 places an obligation on brokers from 1 November 2007 to “execute orders on terms most favourable to the client” - ‘best execution’. Current methods of checking execution quality cannot cope with today’s trading volumes. The only effective method of monitoring hundreds of thousands of trades per week is to have an automated process identifying a sensible set of anomalous trades for examination. Basically, firms need a ‘sifting engine’ that identifies potentially anomalous trades – “best execution compliance automation”.

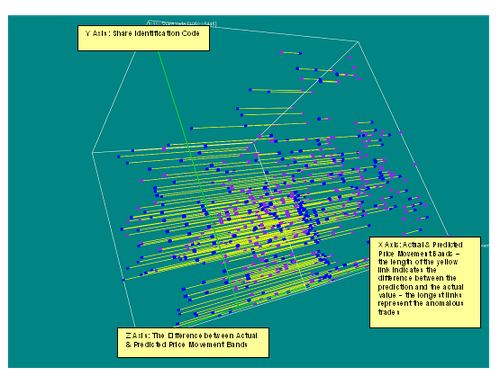

Z/Yen, in co-operation with Sun Microsystems, the London Stock Exchange and four leading brokers, has just completed a large research study to trial PropheZy, a commercial application of a support vector machine, as an anomalous trade detector. Using three months of data comprising over 190,000 trades with a value of over £54bn in order to predict a fourth month, the objective was to see if PropheZy could predict the likely price range of a trade (specifically one of twenty price movement bands, based on a logarithmic scale).

The project proved that PropheZy successfully predicted price movement bands. Setting the level of acceptable accuracy at “within 0 to 4 bands” out of 20, PropheZy was able to predict over 50% of the trades price bands acceptably. Using these predictions, it was possible to set a level for best execution anomalies using price band prediction differences. If trades executed at ‘best’ price (or better) are excluded from the anomalous trades, the number of anomalies is reduced to approximately 1%. Participating brokers concluded that the system was providing trades worthy of investigation:

“This system would be a great way of seeing a small number of ‘odd looking’ trades that we could check - the fact that the same principles could be applied to fixed income and other instruments makes it particularly interesting”.

“I was fascinated to see the selection of trades that this system identified – there were good reasons why all of them traded at the prices shown but they were just the sort of trades that we should have been looking at”.

The instruments covered by this system could be extended, with further testing, to derivatives, commodities, foreign exchange and other markets. Exchanges might wish to provide an automated, centralised compliance service for their members. During the course of the project the team built a prototype “Compliance Workstation” combining a number of tools (PropheZy, VizZy, FractalIntelligence and Decisionality within an Excel framework) that spots anomalies and visualises them, allowing a compliance officer to ‘drill down’ for detailed examination with an appropriate ‘audit trail’.

Professor Michael Mainelli, Chairman of Z/Yen Limited, said:

“This project’s results are very exciting because they show that the automated sifting of trades can identify anomalies, thus reducing the costs of complying with MiFID while simultaneously increasing the effectiveness of the compliance function”.

The research is due to be published in June 2006 in the Journal of Risk Finance in two parts:

- Michael Mainelli and Mark Yeandle, "Best Execution Compliance Automation, Towards An Equities Compliance Workstation" (PDF), Journal of Risk Finance, Emerald Group Publishing Limited (June 2006).

- Michael Mainelli and Mark Yeandle, "Best Execution Compliance, New Techniques for Managing Compliance Risk" (PDF), Journal of Risk Finance, Emerald Group Publishing Limited (June 2006).

For further information or a more detailed summary of this research please contact either Michael Mainelli or Mark Yeandle on +44 (0)20 7562-9562.

Z/Yen specialises in risk/reward management, an innovative approach to improving organisational performance. Z/Yen’s clients include blue chip companies in banking, technology and professional services as well as charities, government and care organisations (see www.zyen.com).

PropheZy won a 2003 DTI Smart Award for risk/reward prediction in numerous markets. More information on PropheZy and VizZy is available on the Z/Yen website.